Extractive Commodity Trading Report 2023

|

Download the Report (pdf) ➥ English Quick access → Key Findings & Recommendations → Scoring framework → Document library |

Overview

The trading of extractive commodities (oil and gas, metals and minerals) is of huge importance, not only in maintaining global flows of these resources but also in providing many resource-rich countries with critical revenues for their economic development. Recent events have underscored the interconnections between the commodity trading sector and sustainable development. This is seen for example in the commodity market disruption caused by the Covid-19 pandemic and the sanctions imposed by some countries since the start of the war in Ukraine, and in recent high-profile cases of bribery and corruption within the sector.

Governments, financiers, customers and consumers are showing increased awareness of the need for the commodity trading industry to demonstrate more systematic action and transparency on economic, environmental, social and governance issues if internationally agreed aims on human rights, sustainable development and accountable financial flows are to be achieved – including the UN Sustainable Development Goals.

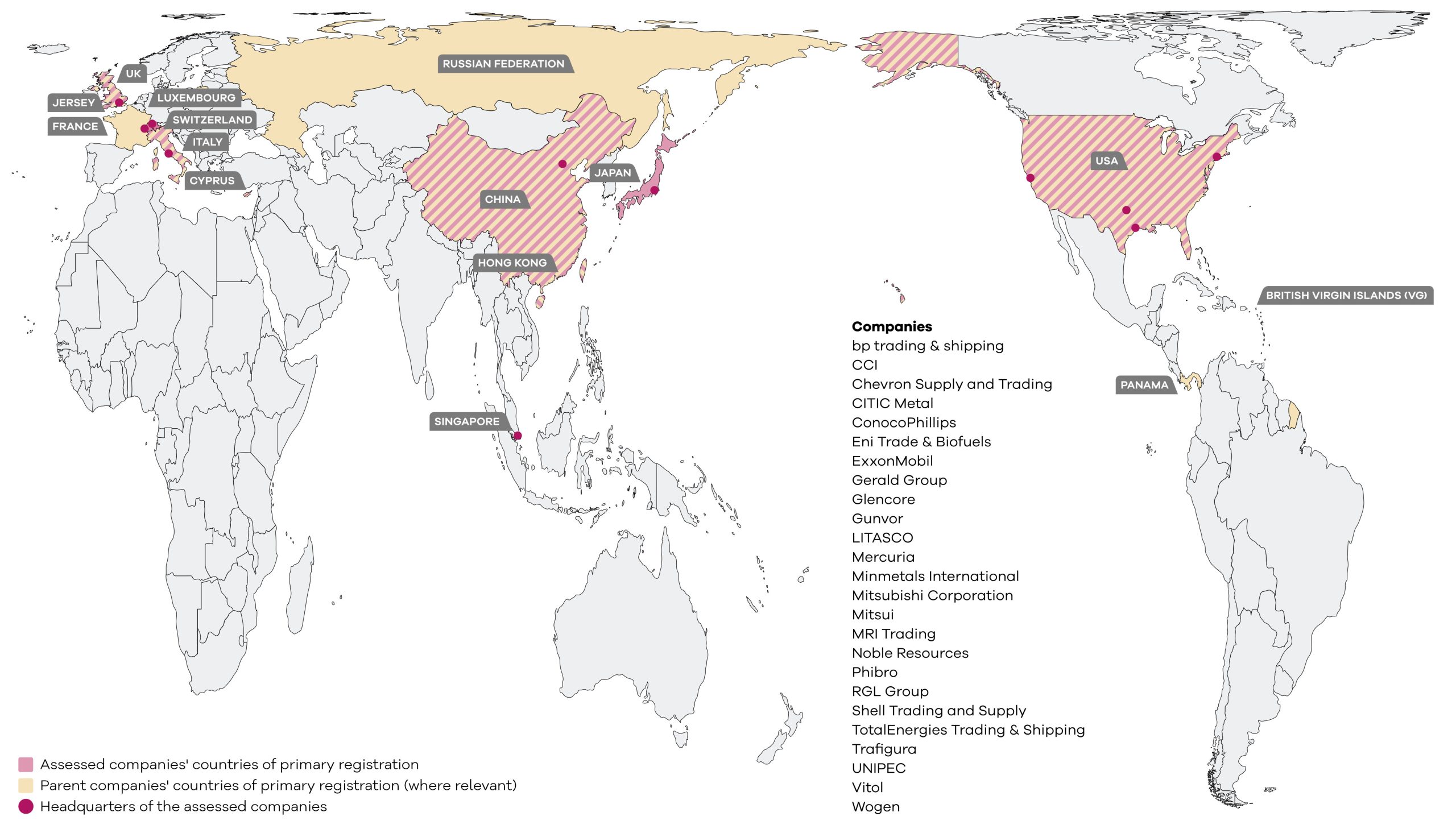

The Extractive Commodity Trading Report (ECTR) 2023 is an evidence-based assessment of due diligence and public disclosure among a sample of companies in the extractive commodity trading sector. Coming two years after the first edition of the assessment, the Report continues to track, and encourage improvement in, companies’ policies and practices related to responsible sourcing and public data sharing.

The 25 geographically dispersed companies included in the assessment have significant activities in the trade of oil, gas, metals or minerals sourced from third parties, and include traditional trading companies, international oil companies, and integrated companies (involved in both production and trading).

| Companies assessed in the report |

| BP trading & shipping, CCI, Chevron Supply and Trading, CITIC Metal, ConocoPhillips, Eni Trade & Biofuels, ExxonMobil, Gerald Group, Glencore, Gunvor, LITASCO, Mercuria, Minmetals International, Mitsubishi Corporation, Mitsui, MRI Trading, Noble Resources, Phibro, RGL Group, Shell International Trading and Shipping, TotalEnergies Trading & Shipping, Trafigura, UNIPEC, Vitol, and Wogen |

Assessment

| The assessment focuses on issues related to the trading activities of each company, providing an overview of the basic measures that the companies are taking to: (1) manage their supply chain risks related to human rights abuses, illicit financial flows and environmental damage; and (2) publicly share data on their corporate governance, trading activities and other public interest issues. |  |

The assessment results offer companies a ‘gap analysis’ of their current performance, indicating where improvement is most needed. More broadly, the assessment supports industry-wide learning by providing a framework that can be used by all companies in the extractive commodity trading sector and by other stakeholders (e.g., banks, investors, industry associations, etc.) to develop their own approaches on these key issues.

Companies and other stakeholders can use the results, recommendations and learning resources in this report to improve their due diligence and public reporting. For example, the interactive library or over 1,500 documents (sourced largely from the assessed companies) includes useful models of tools such as supplier expectations, risk assessment questionnaires and public reporting frameworks.

The full assessment framework of indicators and metrics is included in the report (See Annex 3).

Key findings & Recommendations

[1] Most due diligence systems fall far short of robust risk management

Most companies’ due diligence systems are very limited, covering little more than the initial step of setting expectations for their suppliers. Few systems extend to the critical stages of assessing supplier compliance, engaging with suppliers, and taking action to address any non-compliance. This is the case for due diligence systems on all three risk areas studied: human rights abuses, illicit financial flows, and environmental damage, with evidence particularly weak on assessment and mitigation of environmental risks. Without these elements the due diligence systems will never contribute to the prevention of these significant supply chain issues.

→ Recommendation: Companies can learn from the few examples of comprehensive due diligence systems demonstrated by some of their peers.

[2] Little effort to improve effectiveness of due diligence systems

Very few companies can show they are checking how well their due diligence measures are working. For example, about two-thirds of the companies show no evidence of tracking and reporting their performance on managing human rights risks in their supply chain. A similar proportion of companies show no evidence of tracking and reporting their performance on preventing illicit financial flows. Given the harmful practices that continue to come to light, particularly on illicit financial flows, the onus is on companies to demonstrate they are reviewing their performance on responsible sourcing and seeking ways to strengthen it.

→ Recommendation: Companies can enhance their continuous improvement efforts by increasing their focus on the last two critical steps of the ‘plan-do-check-act’ management cycle.

[3] Some companies are debunking the myth that public disclosure harms competitiveness

Very few companies are publicly disclosing information of strong public interest such as their annual turnover, the taxes they pay, or their purchases from governments or state-owned enterprises. One of the reasons cited by companies for non-disclosure is that financial data of this kind is highly confidential, and public disclosure could harm their competitiveness. Yet on each of these issues a few companies (private as well as publicly listed) show strong and voluntary disclosure. These good practices demonstrate that transparency on these issues can be considered compatible with competitiveness.

→ Recommendation: Companies can follow the examples of their more transparent peers to share public interest data without compromising their competitiveness.

[4] Anti-bribery and corruption systems rarely supported by practical measures

While most companies have anti-bribery and corruption (ABC) systems, including a compliance function and whistleblowing mechanism, there is less evidence of companies ensuring that their employees routinely fulfil their ABC responsibilities. Few companies show detailed evidence of conducting regular training on ABC for their workforce. And there is no evidence that ABC performance is included in any ESG executive compensation criteria. These kinds of practical measures are critical as ABC risks are by no means hypothetical. Several assessed companies have been subject to recent investigations or legal action relating to bribery and corruption.

→ Recommendation: Companies can improve their prevention of bribery and corruption by strengthening awareness and accountability at all levels of their workforce.

[5] Weak progress overall, some individual improvements

There is no sign of a marked shift towards responsible and transparent practices. The overall average performance has increased only minimally, from 33% to 34% in the last two years. Nonetheless, the majority of companies show progress on at least one issue. Improvements include, for example, new policy commitments, new management standards, and more public sharing of public interest data. Currently a few companies show significantly stronger results among those assessed, and it is encouraging to see that some companies are starting to catch up with their better-performing peers.

→ Recommendation: Companies can use the results of this assessment to improve their due diligence practices and strengthen their public disclosure.

Scoring Framework

Download the full scoring framework

Document Library

This searchable document library includes approximately 1,500 source documents (sourced from the public domain or submitted by companies), which have been reviewed during the assessment of the 25 companies. It is possible to search for a specific text in the titles, using the field below.

| Company | Source document | Year |

|---|---|---|

| bp trading & shipping | BP – 2022 – BP Global Energy Trading, Terms and Conditions (webpage) | 2022 |

| bp trading & shipping | BP – 2022 – Canada 12 Month Lobbying Summary | 2022 |

| bp trading & shipping | BP – 2022 – CDP Climate Change Report | 2022 |

| bp trading & shipping | BP – 2022 – Corporate Governance (webpage) | 2022 |

| bp trading & shipping | BP – 2022 – Five aims to get bp to net zero (webpage) | 2022 |

| bp trading & shipping | BP – 2022 – Getting to net zero (webpage) | 2022 |

| bp trading & shipping | BP – 2022 – LNG master sales and purchase agreement (webpage) | 2022 |

| bp trading & shipping | BP – 2022 – LNG master sales and purchase agreement (webpage) | 2022 |

| bp trading & shipping | BP – 2022 – Our participation in trade associations climate review | 2022 |

| bp trading & shipping | BP – 2022 – Q2 US Senate Lobbying Disclosure | 2022 |

| bp trading & shipping | BP – 2022 – Tax Transparency (webpage) | 2022 |

| bp trading & shipping | BP – 2022 – Terms and conditions (T&Cs) Documents and downloads bp trading & shipping (webpage) | 2022 |

| bp trading & shipping | BP – 2022 – Texas Fact Sheet | 2022 |

| bp trading & shipping | BP – 2022 – Trading & Shipping (webpage) | 2022 |

| bp trading & shipping | BP – 2022 – trading and shipping offices (webpage) | 2022 |

| bp trading & shipping | BP – 2022 – UNGC communication on progress | 2022 |

| bp trading & shipping | BP – 2022 – What we do bp Trading & Shipping (webpage) | 2022 |

| bp trading & shipping | BP – 2021 – Annual Report and Form 20-F | 2021 |

| bp trading & shipping | BP – 2021 – Environmental Policy | 2021 |

| bp trading & shipping | BP – 2021 – ESG Datasheet | 2021 |

| bp trading & shipping | BP – 2021 – Governance Report | 2021 |

| bp trading & shipping | BP – 2021 – Modern slavery and human trafficking statement | 2021 |

| bp trading & shipping | BP – 2021 – Our Responsible Tax Principles | 2021 |

| bp trading & shipping | BP – 2021 – Report on Payments to Governments | 2021 |

| bp trading & shipping | BP – 2021 – Sustainability Report | 2021 |

| bp trading & shipping | BP – 2021 – Terms of reference Safety and sustainability committee | 2021 |

| bp trading & shipping | BP – 2020 – Answers to Clarification Questions | 2020 |

| bp trading & shipping | BP – 2020 – Business and human rights policy | 2020 |

| bp trading & shipping | BP – 2020 – EU Transparency Register – List of Meetings with European Commission since 2014 | 2020 |

| bp trading & shipping | BP – 2020 – EU Transparency Register (webpage) | 2020 |

| bp trading & shipping | BP – 2020 – Organization chart | 2020 |

| bp trading & shipping | BP – 2020 – Our participation in trade association, Climate | 2020 |

| bp trading & shipping | BP – BP America – 2020 – US House of Representative Lobbying Disclosure, 2nd quarter | 2020 |

| bp trading & shipping | BP – BP Canada Limited – 2020 – Office of the Commissioner of Lobbying of Canada – 12 month Lobbying Activity | 2020 |

| bp trading & shipping | BP – BP Global Oil Americas – 2020 – General Terms and Conditions for Purchases and Sales of Crude Oil, Refined Petroleum and Related Products | 2020 |

| bp trading & shipping | BP – BP Global Oil Americas – 2020 – Marine Provisions | 2020 |

| bp trading & shipping | BP – BP Global Oil Americas – 2020 – Pipeline and Tank Provisions | 2020 |

| bp trading & shipping | BP – BP Global Oil Americas – 2020 – RINs Provisions | 2020 |

| bp trading & shipping | BP – BP Global Oil Americas – 2020 – Truck and Rail Provisions | 2020 |

| bp trading & shipping | BP – 2020 – Sustainability Report | 2020 |

| bp trading & shipping | BP – 2020 – Tax Report | 2020 |

| bp trading & shipping | BP – 2019 – Annual report and Form 20-F | 2019 |

| bp trading & shipping | BP – 2019 – BP Global energy trading, FOB LNG sale and purchase agreement | 2019 |

| bp trading & shipping | BP – 2019 – BP Global energy trading, Master ex-ship LNG sale and purchase agreement | 2019 |

| bp trading & shipping | BP – 2019 – BP’s approach to tax | 2019 |

| bp trading & shipping | BP – 2019 – ESG Data Sheet | 2019 |

| bp trading & shipping | BP – 2019 – Labour Rights & Modern Slavery Principles | 2019 |

| bp trading & shipping | BP – 2019 – Report on payments to governments | 2019 |

| bp trading & shipping | BP – 2019 – Slavery and human trafficking statement | 2019 |

| bp trading & shipping | BP – 2019 – Sustainability Report | 2019 |

| bp trading & shipping | BP – Britannic Energy Trading Limited – 2019 – Annual Report and Financial Statements | 2019 |

| bp trading & shipping | International Swaps and Derivatives Association – 2019 – Disclosure Annex for Commodity Derivative Transactions | 2019 |

| bp trading & shipping | International Swaps and Derivatives Association – 2019 – General Disclosure Statement for Transactions | 2019 |

| bp trading & shipping | BP – 2019 – BP’s expectations of its suppliers | 2019 |

| bp trading & shipping | BP – 2018 – BP Global energy trading, Terms and Conditions of Sale Marine Fuels | 2018 |

| bp trading & shipping | BP – 2017 – BP’s expectation of its suppliers | 2017 |

| bp trading & shipping | BP – 2016 – BP Global energy trading, Additional Disclosure Statement for Complex Structures | 2016 |

| bp trading & shipping | BP – BP Oil International Ltd – 2015 – General terms & Conditions for Sales and Purchases of Crude oil and Petroleum Products | 2015 |

| bp trading & shipping | BP – BP Energy Company – nd – Code of Conduct for persons engaged in natural gas sale | nd |

| bp trading & shipping | BP – nd – A list of frequently asked questions relating to ESG topics (webpage) | nd |

| bp trading & shipping | BP – nd – Anti-bribery and corruption (webpage) | nd |

| bp trading & shipping | BP – nd – Board Governance Principles | nd |

| bp trading & shipping | BP – nd – BP and our people (webpage) | nd |

| bp trading & shipping | BP – nd – BP Global energy trading, About us (webpage) | nd |

| bp trading & shipping | BP – nd – BP Global energy trading, Americas (webpage) | nd |

| bp trading & shipping | BP – nd – BP Global energy trading, Central Asia (webpage) | nd |

| bp trading & shipping | BP – nd – BP Global energy trading, Corporate Power Purchase Agreements (PPAs) | nd |

| bp trading & shipping | BP – nd – BP Global energy trading, Europe (webpage) | nd |

| bp trading & shipping | BP – nd – BP Global energy trading, European Gas and Power (webpage) | nd |

| bp trading & shipping | BP – nd – BP Global energy trading, European Gas and Power brochure | nd |

| bp trading & shipping | BP – nd – BP Global energy trading, European Gas and Power Purchase Agreements (webpage) | nd |

| bp trading & shipping | BP – nd – BP Global energy trading, Far East (webpage) | nd |

| bp trading & shipping | BP – nd – BP Global energy trading, Gas and Power (webpage) | nd |

| bp trading & shipping | BP – nd – BP Global energy trading, General terms and conditions (webpage) | nd |

| bp trading & shipping | BP – nd – BP Global energy trading, Generic renewable PPA Structure | nd |

| bp trading & shipping | BP – nd – BP Global energy trading, Global environmental products (webpage) | nd |

| bp trading & shipping | BP – nd – BP Global energy trading, Global structured products (webpage) | nd |

| bp trading & shipping | BP – nd – BP Global energy trading, Global Structured Products brochure | nd |

| bp trading & shipping | BP – nd – BP Global energy trading, Greenfield LNG brochure | nd |

| bp trading & shipping | BP – nd – BP Global energy trading, Liquefied natural gas Asia Middle East (webpage) | nd |

| bp trading & shipping | BP – nd – BP Global energy trading, Liquefied natural gas Europe (webpage) | nd |

| bp trading & shipping | BP – nd – BP Global energy trading, LNG brochure | nd |

| bp trading & shipping | BP – nd – BP Global energy trading, LNG master sales and purchase agreement (webpage) | nd |

| bp trading & shipping | BP – nd – BP Global energy trading, Marine (webpage) | nd |

| bp trading & shipping | BP – nd – BP Global energy trading, Marine brochure | nd |

| bp trading & shipping | BP – nd – BP Global energy trading, Middle East (webpage) | nd |

| bp trading & shipping | BP – nd – BP Global energy trading, Natural gas liquids (webpage) | nd |

| bp trading & shipping | BP – nd – BP Global energy trading, North Africa (webpage) | nd |

| bp trading & shipping | BP – nd – BP Global energy trading, Oil (webpage) | nd |

| bp trading & shipping | BP – nd – BP Global energy trading, Regulatory resource centre (webpage) | nd |

| bp trading & shipping | BP – nd – BP Global energy trading, West Africa (webpage) | nd |

| bp trading & shipping | BP – nd – Community Engagement (webpage) | nd |

| bp trading & shipping | BP – nd – Global energy trading (webpage) | nd |

| bp trading & shipping | BP – nd – Human Rights Policy (webpage) | nd |

| bp trading & shipping | BP – nd – Key sustainability issues (webpage) | nd |

| bp trading & shipping | BP – nd – Labour rights (webpage) | nd |

| bp trading & shipping | BP – nd – Local workers and suppliers (webpage) | nd |

| bp trading & shipping | BP – nd – Managing risks (webpage) | nd |

| bp trading & shipping | BP – nd – Open Talk (webpage) | nd |

| bp trading & shipping | BP – nd – Our business model (webpage) | nd |

| bp trading & shipping | BP – nd – Our code our responsibility | nd |

| bp trading & shipping | BP – nd – Our impacts on communities (webpage) | nd |

| bp trading & shipping | BP – nd – Personal Safety (webpage) | nd |

| bp trading & shipping | BP – nd – Policy and advocacy (webpage) | nd |

| bp trading & shipping | BP – nd – Responsible supply chain management (webpage) | nd |

| bp trading & shipping | BP – nd – Running a responsible business (webpage) | nd |

| bp trading & shipping | BP – nd – Stakeholders engagement (webpage) | nd |

| bp trading & shipping | BP – nd – Supplier expectations (webpage) | nd |

| bp trading & shipping | BP – nd – Sustainability Governance (webpage) | nd |

| bp trading & shipping | BP – nd – Tax Transparency (webpage) | nd |

| bp trading & shipping | BP – nd – UN Sustainable Development Goals (webpage) | nd |

| CCI | CCI – 2022 – Assets Natural Gas (webpage) | 2022 |

| CCI | CCI – 2022 – Assets Other (webpage) | 2022 |

| CCI | CCI – 2022 – Assets Power (webpage) | 2022 |

| CCI | CCI – 2022 – Contact Us (webpage) | 2022 |

| CCI | CCI – 2022 – History (webpage) | 2022 |

| CCI | CCI – 2022 – Leadership Team (webpage) | 2022 |

| CCI | CCI – 2022 – Life at CCI (webpage) | 2022 |

| CCI | CCI – 2022 – Locations (webpage) | 2022 |

| CCI | CCI – 2022 – Natural Gas (webpage) | 2022 |

| CCI | CCI – 2022 – Oil (webpage) | 2022 |

| CCI | CCI – 2022 – Power (webpage) | 2022 |

| CCI | CCI – 2022 – Responsibility (webpage) | 2022 |

| CCI | CCI – 2022 – UK Regulatory Notices (webpage) | 2022 |

| CCI | CCI – 2018 – General terms and conditions for the sale of crude oil and Petroleum products | 2018 |

| Chevron Supply and Trading | Chevron – 2022 – Approach to tax | 2022 |

| Chevron Supply and Trading | Chevron – 2022 – Business conduct and ethics code | 2022 |

| Chevron Supply and Trading | Chevron – 2022 – Chevron hotline (webpage) | 2022 |

| Chevron Supply and Trading | Chevron – 2022 – Form 10-K | 2022 |

| Chevron Supply and Trading | Chevron – 2022 – Form SD Conflict Minerals Disclosure | 2022 |

| Chevron Supply and Trading | Chevron – 2022 – Human rights (webpage) | 2022 |

| Chevron Supply and Trading | Chevron – 2022 – Lobbying and trade associations | 2022 |

| Chevron Supply and Trading | Chevron – 2022 – Proxy statement | 2022 |

| Chevron Supply and Trading | Chevron – 2022 – Supply and trading (webpage) | 2022 |

| Chevron Supply and Trading | Chevron – 2022 – Supply chain management (webpage) | 2022 |

| Chevron Supply and Trading | Chevron – Chevron Belgium BV – 2022 – EU Transparency Register (webpage) | 2022 |

| Chevron Supply and Trading | Chevron – Chevron Belgium BV – 2022 – EU Transparency Register, List of Meetings with the European Commission since 2014 | 2022 |

| Chevron Supply and Trading | Chevron – Chevron Canada Limited – 2022 – Registry of Lobbyists, Office of the Commissioner of Lobbying of Canada, Version 68 of 68 | 2022 |

| Chevron Supply and Trading | Chevron – Chevron USA – 2022 – US House of Representatives, Lobbying disclosure 2nd quarter | 2022 |

| Chevron Supply and Trading | Chevron – 2022 – Pipelines (webpage) | 2022 |

| Chevron Supply and Trading | Chevron – 2021 – Annual Report | 2021 |

| Chevron Supply and Trading | Chevron – 2021 – Climate change resilience report | 2021 |

| Chevron Supply and Trading | Chevron – 2021 – Corporate sustainability report | 2021 |

| Chevron Supply and Trading | Chevron – 2021 – Expectations for suppliers, contractors and business partners | 2021 |

| Chevron Supply and Trading | Chevron – 2021 – United Kingdom Modern Slavery Act Statement for 2021 | 2021 |

| Chevron Supply and Trading | Chevron – 2020 – Answers to Clarification Questions | 2020 |

| Chevron Supply and Trading | Chevron – 2020 – Approach to tax | 2020 |

| Chevron Supply and Trading | Chevron – 2020 – Business Conduct and Ethics Code | 2020 |

| Chevron Supply and Trading | Chevron – 2020 – Proxy statement, Notice of meeting of shareholders | 2020 |

| Chevron Supply and Trading | Chevron – 2020 – Supplier letter expectations for suppliers, contractors and business partners | 2020 |

| Chevron Supply and Trading | Chevron – Chevron Belgium BVBA – 2020 – EU Transparency Register (webpage) | 2020 |

| Chevron Supply and Trading | Chevron – Chevron Belgium BVBA – 2020 – EU Transparency Register, List of Meetings with European Commission since 2014 | 2020 |

| Chevron Supply and Trading | Chevron – Chevron Canada Limited – 2020 – Office of the Commissioner of Lobbying of Canada, 12 month lobbying summary | 2020 |

| Chevron Supply and Trading | Chevron – Chevron USA – 2020 – US House of Representative, Lobbying Disclosure 2nd quarter | 2020 |

| Chevron Supply and Trading | Chevron – 2020 – Stewarding responsible water management | 2020 |

| Chevron Supply and Trading | Chevron – 2019 – Annual Report | 2019 |

| Chevron Supply and Trading | Chevron – 2019 – Annual Report Supplement | 2019 |

| Chevron Supply and Trading | Chevron – 2019 – Employees Political Action Committee Contributions | 2019 |

| Chevron Supply and Trading | Chevron – 2019 – Form 10-K, Annual Report | 2019 |

| Chevron Supply and Trading | Chevron – 2019 – Form SD Conflict Minerals Disclosure | 2019 |

| Chevron Supply and Trading | Chevron – 2019 – Human Right Policy | 2019 |

| Chevron Supply and Trading | Chevron – 2019 – Lloyd’s Register LRQA Assurance Statement ISO 14001 and OHSAS 18001 | 2019 |

| Chevron Supply and Trading | Chevron – 2019 – Political Contributions Report | 2019 |

| Chevron Supply and Trading | Chevron – 2019 – Public Policy Committee Charter | 2019 |

| Chevron Supply and Trading | Chevron – 2019 – Statement on Human Rights Defenders | 2019 |

| Chevron Supply and Trading | Chevron – 2019 – Sustainability Report | 2019 |

| Chevron Supply and Trading | Chevron – 2019 – Trade association memberships with annual dues of USD 100 000+ | 2019 |

| Chevron Supply and Trading | Chevron – 2019 – Update to the Climate Change Resilience, a framework for resilience making | 2019 |

| Chevron Supply and Trading | Chevron – Chevron Canada – 2019 – Disclosure Extractive Sector Transparency Measures Act | 2019 |

| Chevron Supply and Trading | Chevron – 2018 – Climate Change Resilience, a framework for resilience making | 2018 |

| Chevron Supply and Trading | Chevron – 2018 – General terms & conditions for sales and purchases of Crude Oil US Domestic Supplement | 2018 |

| Chevron Supply and Trading | Chevron – 2018 – General terms & conditions for sales and purchases of Products US Domestic Supplement | 2018 |

| Chevron Supply and Trading | Chevron – 2018 – Notice Regarding Updated Corporation Business Conduct and Ethics Code | 2018 |

| Chevron Supply and Trading | Chevron – 2018 – Summary Grievance Mechanism Guidance | 2018 |

| Chevron Supply and Trading | Chevron – 2017 – Modern Slavery, Human Trafficking and Broader Human Rights Commitments California Transparency in Supply Chains Act of 2010 | 2017 |

| Chevron Supply and Trading | Chevron – 2016 – Responsible Investment in Myanmar | 2016 |

| Chevron Supply and Trading | Chevron – 2014 – General terms & conditions for sales and purchases of crude oil (version 2) | 2014 |

| Chevron Supply and Trading | Chevron – 2014 – General terms & conditions for sales and purchases of products (version 2) | 2014 |

| Chevron Supply and Trading | Chevron – 2014 – Global Operations, One Approach | 2014 |

| Chevron Supply and Trading | Chevron – Chevron Natural Gas – nd – Code of Conduct | nd |

| Chevron Supply and Trading | Chevron – nd – About Crude Oil Marketing (webpage) | nd |

| Chevron Supply and Trading | Chevron – nd – An overview for the workforce, Operational excellence Managing safeguards to protect people and the environment | nd |

| Chevron Supply and Trading | Chevron – nd – Audit Committee Charter | nd |

| Chevron Supply and Trading | Chevron – nd – Business Conduct and Ethics Expectations for Suppliers and Contractors | nd |

| Chevron Supply and Trading | Chevron – nd – Chevron Crude Oil Marketing, African Crudes (webpage) | nd |

| Chevron Supply and Trading | Chevron – nd – Chevron Crude Oil Marketing, Central Asian Crudes (webpage) | nd |

| Chevron Supply and Trading | Chevron – nd – Chevron Crude Oil Marketing, Crude Oils (webpage) | nd |

| Chevron Supply and Trading | Chevron – nd – Chevron Crude Oil Marketing, European Crudes (webpage) | nd |

| Chevron Supply and Trading | Chevron – nd – Chevron Crude Oil Marketing, Far Eastern Crudes (webpage) | nd |

| Chevron Supply and Trading | Chevron – nd – Chevron Crude Oil Marketing, Latin American Crudes (webpage) | nd |

| Chevron Supply and Trading | Chevron – nd – Chevron Crude Oil Marketing, Middle Eastern Crudes (webpage) | nd |

| Chevron Supply and Trading | Chevron – nd – Chevron Crude Oil Marketing, North American Crudes (webpage) | nd |

| Chevron Supply and Trading | Chevron – nd – Ethics Point (webpage) | nd |

| Chevron Supply and Trading | Chevron – nd – Frequent Questions Hotline | nd |

| Chevron Supply and Trading | Chevron – nd – Governance (webpage) | nd |

| Chevron Supply and Trading | Chevron – nd – Human Rights (webpage) | nd |

| Chevron Supply and Trading | Chevron – nd – Human Rights (webpage) | nd |

| Chevron Supply and Trading | Chevron – nd – Operational Excellence Management System (OEMS) | nd |

| Chevron Supply and Trading | Chevron – nd – Operational Excellence Management System (webpage) | nd |

| Chevron Supply and Trading | Chevron – nd – Political Contributions and Lobbying (webpage) | nd |

| Chevron Supply and Trading | Chevron – nd – Respecting human rights, Enabling human progress begins with respecting human rights | nd |

| Chevron Supply and Trading | Chevron – nd – Supplier diversity (webpage) | nd |

| Chevron Supply and Trading | Chevron – nd – Supply and trading (webpage) | nd |

| Chevron Supply and Trading | Chevron – nd – Supply Chain Management (webpage) | nd |

| Chevron Supply and Trading | Chevron – nd – The Chevron Way | nd |

| Chevron Supply and Trading | Chevron – nd – United Kingdom (webpage) | nd |

| Chevron Supply and Trading | EITI – nd – Data Portal (webpage) | nd |

| Chevron Supply and Trading | Chevron – nd – California Transparency in Supply Chains Act Disclosure | nd |

| Chevron Supply and Trading | Chevron – nd – Chevron’s approach to UK tax | nd |

| CITIC Metal | CITIC – CITIC Metal – 2022 – Commodity Trading, Iron Ore (Chinese) (webpage) | 2022 |

| CITIC Metal | CITIC – CITIC Metal – 2022 – Commodity Trading, Iron Ore (webpage) | 2022 |

| CITIC Metal | CITIC – CITIC Metal – 2022 – Commodity Trading, Niobium (Chinese) (webpage) | 2022 |

| CITIC Metal | CITIC – CITIC Metal – 2022 – Commodity Trading, Niobium (webpage) | 2022 |

| CITIC Metal | CITIC – CITIC Metal – 2022 – Commodity Trading, Non-Ferrous Metals (Chinese) (webpage) | 2022 |

| CITIC Metal | CITIC – CITIC Metal – 2022 – Commodity Trading, Non-Ferrous Metals (webpage) | 2022 |

| CITIC Metal | CITIC – CITIC Metal – 2022 – Commodity Trading, Special Ores (Chinese) (webpage) | 2022 |

| CITIC Metal | CITIC – CITIC Metal – 2022 – Commodity Trading, Special Ores (webpage) | 2022 |

| CITIC Metal | CITIC – CITIC Resources – 2022 – Import and Export of Commodities (Chinese) (webpage) | 2022 |

| CITIC Metal | CITIC – CITIC Resources – 2022 – Import and Export of Commodities (webpage) | 2022 |

| CITIC Metal | CITIC – 2021 – Annual Report | 2021 |

| CITIC Metal | CITIC – 2021 – Annual Report (Chinese) | 2021 |

| CITIC Metal | CITIC – CITIC Resources – 2021 – Annual Report | 2021 |

| CITIC Metal | CITIC – CITIC Resources – 2021 – Annual Report (Chinese) | 2021 |

| CITIC Metal | CITIC – CITIC Resources – 2021 – Environmental Social and Governance Report | 2021 |

| CITIC Metal | CITIC – CITIC Resources – 2021 – Environmental Social and Governance Report (Chinese) | 2021 |

| CITIC Metal | CITIC – CITIC Resources – 2020 – Chairman’s Statement (Chinese) (webpage) | 2020 |

| CITIC Metal | CITIC – CITIC Resources – 2020 – Chairman’s Statement (webpage) | 2020 |

| CITIC Metal | CITIC – 2020 – Annual Report | 2020 |

| CITIC Metal | CITIC – 2020 – Annual Report (Chinese) | 2020 |

| CITIC Metal | CITIC – CITIC Resources – 2020 – Annual Report | 2020 |

| CITIC Metal | CITIC – CITIC Resources – 2020 – Annual Report (Chinese) | 2020 |

| CITIC Metal | CITIC – CITIC Resources – 2020 – Environmental Social and Governance Report | 2020 |

| CITIC Metal | CITIC – CITIC Resources – 2020 – Environmental Social and Governance Report (Chinese) | 2020 |

| CITIC Metal | CITIC – 2019 – Annual Report | 2019 |

| CITIC Metal | CITIC – 2019 – Annual Report (Chinese) | 2019 |

| CITIC Metal | CITIC – 2019 – Half-Year Report | 2019 |

| CITIC Metal | CITIC – 2019 – Half-Year Report (Chinese) | 2019 |

| CITIC Metal | CITIC – CITIC Resources – 2019 – Annual Report | 2019 |

| CITIC Metal | CITIC – CITIC Resources – 2019 – Annual Report (Chinese) | 2019 |

| CITIC Metal | CITIC – CITIC Resources – 2019 – Environmental Social and Governance Report | 2019 |

| CITIC Metal | CITIC – CITIC Resources – 2019 – Environmental Social and Governance Report (Chinese) | 2019 |

| CITIC Metal | CITIC – CITIC Resources – 2019 – Interim Report | 2019 |

| CITIC Metal | CITIC – CITIC Resources – 2019 – Interim Report (Chinese) | 2019 |

| CITIC Metal | CITIC – 2013 – Board Diversity Policy | 2013 |

| CITIC Metal | CITIC – 2013 – Board Diversity Policy (Chinese) | 2013 |

| CITIC Metal | CITIC – CITIC Resources – 2013 – By-Laws | 2013 |

| CITIC Metal | CITIC – 2012 – Inside Information Disclosure Policy | 2012 |

| CITIC Metal | CITIC – 2012 – Inside Information Disclosure Policy (Chinese) | 2012 |

| CITIC Metal | CITIC – 2012 – Shareholders Communication Policy | 2012 |

| CITIC Metal | CITIC – 2012 – Shareholders Communication Policy (Chinese) | 2012 |

| CITIC Metal | CITIC – CITIC Metal – nd – About CMG (Chinese) (webpage) | nd |

| CITIC Metal | CITIC – CITIC Metal – nd – About CMG (webpage) | nd |

| CITIC Metal | CITIC – CITIC Metal – nd – Commodity Trading, Coal (Chinese) (webpage) | nd |

| CITIC Metal | CITIC – CITIC Metal – nd – Commodity Trading, Coal (webpage) | nd |

| CITIC Metal | CITIC – CITIC Metal – nd – Commodity Trading, Iron Ore (Chinese) (webpage) | nd |

| CITIC Metal | CITIC – CITIC Metal – nd – Commodity Trading, Iron Ore (webpage) | nd |

| CITIC Metal | CITIC – CITIC Metal – nd – Commodity Trading, Niobium (Chinese) (webpage) | nd |

| CITIC Metal | CITIC – CITIC Metal – nd – Commodity Trading, Niobium (webpage) | nd |

| CITIC Metal | CITIC – CITIC Metal – nd – Commodity Trading, Non-Ferrous Metals (Chinese) (webpage) | nd |

| CITIC Metal | CITIC – CITIC Metal – nd – Commodity Trading, Non-Ferrous Metals (webpage) | nd |

| CITIC Metal | CITIC – CITIC Metal – nd – Commodity Trading, Special Ores (Chinese) (webpage) | nd |

| CITIC Metal | CITIC – CITIC Metal – nd – Commodity Trading, Special Ores (webpage) | nd |

| CITIC Metal | CITIC – CITIC Metal – nd – Corporate Governance (Chinese) (webpage) | nd |

| CITIC Metal | CITIC – CITIC Metal – nd – Corporate Governance (webpage) | nd |

| CITIC Metal | CITIC – CITIC Metal – nd – Corporate Social Responsibility (Chinese) (webpage) | nd |

| CITIC Metal | CITIC – CITIC Metal – nd – Corporate Social Responsibility (webpage) | nd |

| CITIC Metal | CITIC – CITIC Metal – nd – Shareholding Structure (Chinese) (webpage) | nd |

| CITIC Metal | CITIC – CITIC Metal – nd – Shareholding Structure (webpage) | nd |

| CITIC Metal | CITIC – CITIC Metal – nd – Sustainability (Chinese) (webpage) | nd |

| CITIC Metal | CITIC – CITIC Metal – nd – Sustainability (webpage) | nd |

| CITIC Metal | CITIC – CITIC Resources – nd – Corporate Structure (Chinese) (webpage) | nd |

| CITIC Metal | CITIC – CITIC Resources – nd – Corporate Structure (webpage) | nd |

| CITIC Metal | CITIC – CITIC Resources – nd – Directors and Senior Management (Chinese) (webpage) | nd |

| CITIC Metal | CITIC – CITIC Resources – nd – Directors and Senior Management (webpage) | nd |

| CITIC Metal | CITIC – CITIC Resources – nd – Import and Export of Commodities (Chinese) (webpage) | nd |

| CITIC Metal | CITIC – CITIC Resources – nd – Import and Export of Commodities (webpage) | nd |

| CITIC Metal | CITIC – nd – Corporate Governance (Chinese) (webpage) | nd |

| CITIC Metal | CITIC – nd – Corporate Governance (webpage) | nd |

| CITIC Metal | CITIC – nd – Our Business, Resources & Energy (Chinese) (webpage) | nd |

| CITIC Metal | CITIC – nd – Our Business, Resources & Energy (webpage) | nd |

| CITIC Metal | CITIC – nd – Sustainability (Chinese) (webpage) | nd |

| CITIC Metal | CITIC – nd – Sustainability (webpage) | nd |

| ConocoPhillips | ConocoPhillips – 2022 – CDP Climate Change Report | 2022 |

| ConocoPhillips | ConocoPhillips – 2022 – Committees (webpage) | 2022 |

| ConocoPhillips | ConocoPhillips – 2022 – Ethics Helpline, Commonly asked questions (webpage) | 2022 |

| ConocoPhillips | ConocoPhillips – 2022 – EU Transparency Register (webpage) | 2022 |

| ConocoPhillips | ConocoPhillips – 2022 – EU Transparency Register, List of Meetings since 2014 | 2022 |

| ConocoPhillips | ConocoPhillips – 2022 – Executive Management (webpage) | 2022 |

| ConocoPhillips | ConocoPhillips – 2022 – Global Tax Policy (webpage) | 2022 |

| ConocoPhillips | ConocoPhillips – 2022 – Human Rights Position (webpage) | 2022 |

| ConocoPhillips | ConocoPhillips – 2022 – Operations (webpage) | 2022 |

| ConocoPhillips | ConocoPhillips – 2022 – Proxy Statement | 2022 |

| ConocoPhillips | ConocoPhillips – 2022 – Supplier Expectations (webpage) | 2022 |

| ConocoPhillips | ConocoPhillips – 2022 – US House of Representatives, Lobbying Disclosure 2nd quarter report | 2022 |

| ConocoPhillips | ConocoPhillips – 2022 – Valuing Human Rights (webpage) | 2022 |

| ConocoPhillips | ConocoPhillips – ConocoPhillips Canada Resources Corp – 2022 – Registry of Lobbyists, Office of the Commissioner of Lobbying of Canada, Version 42 of 42 | 2022 |

| ConocoPhillips | ConocoPhillips – ConocoPhillips UK Holdings Limited – 2022 – Statement on Modern Slavery | 2022 |

| ConocoPhillips | ConocoPhillips – 2021 – Annual Report | 2021 |

| ConocoPhillips | ConocoPhillips – 2021 – Annual Report Form 10-K | 2021 |

| ConocoPhillips | ConocoPhillips – 2021 – Public Policy and Sustainability Committee Charter | 2021 |

| ConocoPhillips | ConocoPhillips – 2021 – Sustainability Report | 2021 |

| ConocoPhillips | ConocoPhillips – 2021 – UK Tax Policy | 2021 |

| ConocoPhillips | ConocoPhillips – 2021 – Voluntary Principles on Security and Human Rights, Annual Report | 2021 |

| ConocoPhillips | ConocoPhillips – 2020 – Alaska Factsheet | 2020 |

| ConocoPhillips | ConocoPhillips – 2020 – Canada Factsheet | 2020 |

| ConocoPhillips | ConocoPhillips – 2020 – Code of Business Ethics and Conduct | 2020 |

| ConocoPhillips | ConocoPhillips – 2020 – EU Transparency Register (webpage) | 2020 |

| ConocoPhillips | ConocoPhillips – 2020 – EU Transparency Register, List of Meetings since 2014 | 2020 |

| ConocoPhillips | ConocoPhillips – 2020 – Europe and North Africa Fact Sheet | 2020 |

| ConocoPhillips | ConocoPhillips – 2020 – Lower 48 Factsheet | 2020 |

| ConocoPhillips | ConocoPhillips – 2020 – Other International and Exploration Factsheet | 2020 |

| ConocoPhillips | ConocoPhillips – 2020 – Overview Fact Sheet | 2020 |

| ConocoPhillips | ConocoPhillips – 2020 – Quarterly Report Form 10-Q, Q1 | 2020 |

| ConocoPhillips | ConocoPhillips – 2020 – US House of Representative, Lobbying Disclosure 2nd quarter report | 2020 |

| ConocoPhillips | ConocoPhillips – ConocoPhillips Canada Resources Corp – 2020 – Office of the Commissioner of Lobbying of Canada, 12-Month Lobbying Activity | 2020 |

| ConocoPhillips | ConocoPhillips – ConocoPhillips UK Holdings Limited – 2020 – Statement on Modern Slavery | 2020 |

| ConocoPhillips | ConocoPhillips – 2019 – Annual Report | 2019 |

| ConocoPhillips | ConocoPhillips – 2019 – Annual Report Form 10-K | 2019 |

| ConocoPhillips | ConocoPhillips – 2019 – Asia Pacific and Middle East Factsheet | 2019 |

| ConocoPhillips | ConocoPhillips – 2019 – Audit and Finance Committee Charter | 2019 |

| ConocoPhillips | ConocoPhillips – 2019 – Business and Trade Associations with Membership Dues over $50,000 | 2019 |

| ConocoPhillips | ConocoPhillips – 2019 – ConocoPhillips Corporate Political Contributions | 2019 |

| ConocoPhillips | ConocoPhillips – 2019 – ConocoPhillips Spirit PAC Contributions | 2019 |

| ConocoPhillips | ConocoPhillips – 2019 – Current Report Form 8-K | 2019 |

| ConocoPhillips | ConocoPhillips – 2019 – Environment Social and Governance Highlights | 2019 |

| ConocoPhillips | ConocoPhillips – 2019 – GHG Emissions (webpage) | 2019 |

| ConocoPhillips | ConocoPhillips – 2019 – GHG Emissions Intensity Target (webpage) | 2019 |

| ConocoPhillips | ConocoPhillips – 2019 – Managing Climate-Related Risk | 2019 |

| ConocoPhillips | ConocoPhillips – 2019 – Other ConocoPhillips Political Expenses | 2019 |

| ConocoPhillips | ConocoPhillips – 2019 – Performance by year | 2019 |

| ConocoPhillips | ConocoPhillips – 2019 – Proxy Statement | 2019 |

| ConocoPhillips | ConocoPhillips – 2019 – Quarterly Report Form 10-Q, Q2 | 2019 |

| ConocoPhillips | ConocoPhillips – 2019 – Sustainability Report | 2019 |

| ConocoPhillips | ConocoPhillips – 2019 – UK Tax Policy | 2019 |

| ConocoPhillips | ConocoPhillips – 2019 – Worldwide Operations and Locations | 2019 |

| ConocoPhillips | ConocoPhillips – 2018 – Environment, Social and Governance Highlights | 2018 |

| ConocoPhillips | ConocoPhillips – 2018 – Sustainability Report | 2018 |

| ConocoPhillips | ConocoPhillips – 2018 – Voluntary Principles on Security and Human Rights, Annual Report | 2018 |

| ConocoPhillips | ConocoPhillips – ConocoPhillips UK – nd – Europe Commercial (webpage) | nd |

| ConocoPhillips | ConocoPhillips – nd – Board Oversight (webpage) | nd |

| ConocoPhillips | ConocoPhillips – nd – Business Ethics (webpage) | nd |

| ConocoPhillips | ConocoPhillips – nd – Code of Business Ethics and Conduct | nd |

| ConocoPhillips | ConocoPhillips – nd – Code of Business Ethics and Conduct, Expectations of Suppliers | nd |

| ConocoPhillips | ConocoPhillips – nd – Community Risk Management (webpage) | nd |

| ConocoPhillips | ConocoPhillips – nd – Ethics Helpline, Commonly asked questions (webpage) | nd |

| ConocoPhillips | ConocoPhillips – nd – Executive Management Sustainable Development Oversight (webpage) | nd |

| ConocoPhillips | ConocoPhillips – nd – GHG Target Principles (webpage) | nd |

| ConocoPhillips | ConocoPhillips – nd – Health, Safety & Environment Policy (webpage) | nd |

| ConocoPhillips | ConocoPhillips – nd – Human Rights Due Diligence | nd |

| ConocoPhillips | ConocoPhillips – nd – Human Rights Position (webpage) | nd |

| ConocoPhillips | ConocoPhillips – nd – Key Stakeholders (webpage) | nd |

| ConocoPhillips | ConocoPhillips – nd – Make a Report | nd |

| ConocoPhillips | ConocoPhillips – nd – Managing Sustainable Development Risks (webpage) | nd |

| ConocoPhillips | ConocoPhillips – nd – Organizational Management Sustainable Development Governance (webpage) | nd |

| ConocoPhillips | ConocoPhillips – nd – Political Contributions Policy (webpage) | nd |

| ConocoPhillips | ConocoPhillips – nd – Power in Cooperation, Transportation to Markets (webpage) | nd |

| ConocoPhillips | ConocoPhillips – nd – Public Policy Engagement (webpage) | nd |

| ConocoPhillips | ConocoPhillips – nd – Supplier Expectations (webpage) | nd |

| ConocoPhillips | ConocoPhillips – nd – Supply chain policy | nd |

| ConocoPhillips | ConocoPhillips – nd – Supply Chain Sustainability (webpage) | nd |

| ConocoPhillips | ConocoPhillips – nd – Sustainable Development Governance (webpage) | nd |

| ConocoPhillips | ConocoPhillips – nd – Valuing Human Rights (webpage) | nd |

| ConocoPhillips | ConocoPhillips – nd – Code of Ethics and Business Conduct | nd |

| Eni Trade & Biofuels | ENI – 2022 – Eni Position on Conflict Minerals | 2022 |

| Eni Trade & Biofuels | ENI – 2022 – Eni Trade & Biofuels (webpage) | 2022 |

| Eni Trade & Biofuels | ENI – 2022 – Environmental Protection (webpage) | 2022 |

| Eni Trade & Biofuels | ENI – 2022 – EU Transparency Register | 2022 |

| Eni Trade & Biofuels | ENI – 2022 – EU Transparency Register list of meetings | 2022 |

| Eni Trade & Biofuels | ENI – 2022 – Position on contract transparency (webpage) | 2022 |

| Eni Trade & Biofuels | ENI – 2022 – US Senate Lobbying report | 2022 |

| Eni Trade & Biofuels | ENI – 2022 – Whistleblowing Report (webpage) | 2022 |

| Eni Trade & Biofuels | ENI – Eni Trade & Biofuels – 2022 – HSE Policy (italian) | 2022 |

| Eni Trade & Biofuels | Eni – Eni Trade & Biofuels SpA – 2022 – ETB additional file | 2022 |

| Eni Trade & Biofuels | Eni – Eni Trade & Biofuels SpA – 2022 – Integrative file n.2 | 2022 |

| Eni Trade & Biofuels | Eni – Eni Trade & Biofuels SpA – 2022 – Integrative file n.3 | 2022 |

| Eni Trade & Biofuels | Eni – 2022 – Shareholders and governance (website) | 2022 |

| Eni Trade & Biofuels | ENI – 2021 – Annual Report | 2021 |

| Eni Trade & Biofuels | ENI – 2021 – Annual Report, Form 20F | 2021 |

| Eni Trade & Biofuels | ENI – 2021 – CDP Water security questionnaire | 2021 |

| Eni Trade & Biofuels | ENI – 2021 – Corporate Governance and Shareholding Structure Report 2021 | 2021 |

| Eni Trade & Biofuels | ENI – 2021 – Corporate Governance and Shareholding Structure Report 2021, extract BoD | 2021 |

| Eni Trade & Biofuels | ENI – 2021 – Eni for 2021 a just transition | 2021 |

| Eni Trade & Biofuels | ENI – 2021 – Eni for 2021 carbon neutrality 2050 | 2021 |

| Eni Trade & Biofuels | ENI – 2021 – Eni for 2021 executive summary | 2021 |

| Eni Trade & Biofuels | ENI – 2021 – Eni for 2021 human rights | 2021 |

| Eni Trade & Biofuels | ENI – 2021 – Eni for 2021 human rights, figure p63 | 2021 |

| Eni Trade & Biofuels | ENI – 2021 – Eni for 2021 sustainability performance | 2021 |

| Eni Trade & Biofuels | ENI – 2021 – Form SD Conflict Mineral Disclosure | 2021 |

| Eni Trade & Biofuels | ENI – 2021 – Management system guidelines Anti-Corruption | 2021 |

| Eni Trade & Biofuels | ENI – 2021 – Meetings and activities of the Control and Risk Committee in 2021 | 2021 |

| Eni Trade & Biofuels | ENI – 2021 – Meetings and activities of the Sustainability and Scenarios Committee in 2021 | 2021 |

| Eni Trade & Biofuels | ENI – 2021 – Report on Payments to Governments 2021 | 2021 |

| Eni Trade & Biofuels | ENI – 2021 – Rules of the Sustainability and Scenarios Committee | 2021 |

| Eni Trade & Biofuels | ENI – 2021 – Slavery and Humany Trafficking Statement 2021 | 2021 |

| Eni Trade & Biofuels | Eni – Eni Trade & Biofuels SpA – 2021 – Financial Statement | 2021 |

| Eni Trade & Biofuels | ENI – 2020 – Advice to shareholders of Board of Directors | 2020 |

| Eni Trade & Biofuels | ENI – 2020 – Advice to shareholders of Board of Statutory Auditors | 2020 |

| Eni Trade & Biofuels | ENI – 2020 – Anti-corruption Compliance Program (webpage) | 2020 |

| Eni Trade & Biofuels | ENI – 2020 – Assessment of industry associations’ climate policy positions | 2020 |

| Eni Trade & Biofuels | ENI – 2020 – By-laws | 2020 |

| Eni Trade & Biofuels | ENI – 2020 – Code of Ethics | 2020 |

| Eni Trade & Biofuels | ENI – 2020 – Corporate Governance Model (webpage) | 2020 |

| Eni Trade & Biofuels | ENI – 2020 – ENI For 2020, Human Rights | 2020 |

| Eni Trade & Biofuels | ENI – 2020 – EU Transparency Register (webpage) | 2020 |

| Eni Trade & Biofuels | ENI – 2020 – EU Transparency Register, List of Meetings with European Commission since 2014 | 2020 |

| Eni Trade & Biofuels | ENI – 2020 – Fact Sheet | 2020 |

| Eni Trade & Biofuels | ENI – 2020 – List of Shareholders (webpage) | 2020 |

| Eni Trade & Biofuels | ENI – 2020 – Long-Term Incentive Plan 2020-2022 | 2020 |

| Eni Trade & Biofuels | ENI – 2020 – Management System Guideline, Whistleblowing reports received | 2020 |

| Eni Trade & Biofuels | ENI – 2020 – Managers’ transactions and shareholdings (webpage) | 2020 |

| Eni Trade & Biofuels | ENI – 2020 – Model 231 | 2020 |

| Eni Trade & Biofuels | ENI – 2020 – Position on conflict minerals | 2020 |

| Eni Trade & Biofuels | ENI – 2020 – Presentation, Long-term Strategic Plan to 2050 and 2020-2023 Action Plan | 2020 |

| Eni Trade & Biofuels | ENI – 2020 – Report on remuneration policy and remuneration paid | 2020 |

| Eni Trade & Biofuels | ENI – 2020 – Rules of the Board of Statutory Auditors | 2020 |

| Eni Trade & Biofuels | ENI – 2020 – Rules of the Control and Risk Committee | 2020 |

| Eni Trade & Biofuels | ENI – 2020 – Rules of the Nomination Committee | 2020 |

| Eni Trade & Biofuels | ENI – 2020 – Rules of the Remuneration Committee | 2020 |

| Eni Trade & Biofuels | ENI – 2020 – Rules of the Sustainability and Scenarios Committee | 2020 |

| Eni Trade & Biofuels | ENI – 2020 – US House of Representative, Lobbying Disclosure, 2nd quarter report | 2020 |

| Eni Trade & Biofuels | ENI – ENI Mexico – 2020 – Human Rights Impact Assessment, Area 1 | 2020 |

| Eni Trade & Biofuels | ENI – ENI Trading and Shipping – 2020 – Model 231 (Italian) | 2020 |

| Eni Trade & Biofuels | ENI – ENI Trading and Shipping – 2020 – Responses to Clarification Questions | 2020 |

| Eni Trade & Biofuels | ENI – 2020 – Country by Country Report | 2020 |

| Eni Trade & Biofuels | ENI – Eni Trade & Biofuels – 2020 – Model 231 | 2020 |

| Eni Trade & Biofuels | ENI – 2019 – Annual Report | 2019 |

| Eni Trade & Biofuels | ENI – 2019 – Annual Report, Form 20F | 2019 |

| Eni Trade & Biofuels | ENI – 2019 – Corporate Governance Report | 2019 |

| Eni Trade & Biofuels | ENI – 2019 – ENI For 2019, Carbon Neutrality in the Long Term | 2019 |

| Eni Trade & Biofuels | ENI – 2019 – ENI For 2019, Executive Summary | 2019 |

| Eni Trade & Biofuels | ENI – 2019 – ENI For 2019, Sustainability Performance | 2019 |

| Eni Trade & Biofuels | ENI – 2019 – ESG Data | 2019 |

| Eni Trade & Biofuels | ENI – 2019 – Form SD, Conflict Mineral Disclosure | 2019 |

| Eni Trade & Biofuels | ENI – 2019 – Global Framework Agreement on Industrial Relations and Corporate Social Responsibility | 2019 |

| Eni Trade & Biofuels | ENI – 2019 – Management System Guideline, Antitrust | 2019 |

| Eni Trade & Biofuels | ENI – 2019 – Meetings and activities of the Sustainability and Scenarios Committee in 2019 | 2019 |

| Eni Trade & Biofuels | ENI – 2019 – Remuneration Report | 2019 |

| Eni Trade & Biofuels | ENI – 2019 – Slavery and Human Trafficking Statement | 2019 |

| Eni Trade & Biofuels | ENI – 2019 – Sustainability Report, ENI For 2019, A Just Transition | 2019 |

| Eni Trade & Biofuels | ENI – 2019 – Sustainability Report, ENI For 2019, A Just Transition | 2019 |

| Eni Trade & Biofuels | ENI – 2019 – The Internal Control and Risk Management System (webpage) | 2019 |

| Eni Trade & Biofuels | ENI – ENI Angola – 2019 – Human Rights Assessment, Cabinda North | 2019 |

| Eni Trade & Biofuels | ENI – ENI Mexico – 2019 – Human Rights Action Plan, Area 1 | 2019 |

| Eni Trade & Biofuels | ENI – ENI Trading and Shipping – 2019 – Sensitive Activities and Specific Control Standards of Model 231 (Italian) | 2019 |

| Eni Trade & Biofuels | ENI – ENI Trading and Shipping – 2019 – Financial Statement 2019 (short version) | 2019 |

| Eni Trade & Biofuels | WBCSD – 2019 – CEO Guide to Human Rights | 2019 |

| Eni Trade & Biofuels | ENI – 2018 – Corporate Governance Code | 2018 |

| Eni Trade & Biofuels | ENI – 2018 – Country by Country Report | 2018 |

| Eni Trade & Biofuels | ENI – 2018 – Fact Book | 2018 |

| Eni Trade & Biofuels | ENI – 2018 – Report on Payments to Governments | 2018 |

| Eni Trade & Biofuels | ENI – 2018 – Tax Strategy | 2018 |

| Eni Trade & Biofuels | ENI – 2017 – Management System Guideline, Transaction with related parties | 2017 |

| Eni Trade & Biofuels | ENI – 2014 – Management System Guideline, Anti-Corruption | 2014 |

| Eni Trade & Biofuels | ENI – 2011 – Sustainability Policy | 2011 |

| Eni Trade & Biofuels | ENI – ENI Myanmar – nd – Human Rights Report, Block RSF-5 | nd |

| Eni Trade & Biofuels | ENI – ENI Trading and Shipping – nd – Articles of Association (Italian) | nd |

| Eni Trade & Biofuels | ENI – ENI Trading and Shipping – nd – Corporate Structure | nd |

| Eni Trade & Biofuels | ENI – ENI Trading and Shipping – nd – Integrative File #2 for RMF Assessment | nd |

| Eni Trade & Biofuels | ENI – ENI Trading and Shipping – nd – Integrative File for Responsible Mining Foundation Assessment | nd |

| Eni Trade & Biofuels | ENI – nd – Biodiversity and Ecosystem Services Policy | nd |

| Eni Trade & Biofuels | ENI – nd – Board of Directors (webpage) | nd |

| Eni Trade & Biofuels | ENI – nd – Board Secretary and Corporate Governance Counsel Charter | nd |

| Eni Trade & Biofuels | ENI – nd – Commitment to Respect Human Rights (webpage) | nd |

| Eni Trade & Biofuels | ENI – nd – Eni Space, Home Page (webpage) | nd |

| Eni Trade & Biofuels | ENI – nd – Eni’s proposals on corporate governance | nd |

| Eni Trade & Biofuels | ENI – nd – Eni’s management of whistleblowing reports (webpage) | nd |

| Eni Trade & Biofuels | ENI – nd – Environmental Protection (webpage) | nd |

| Eni Trade & Biofuels | ENI – nd – FAQs on Board of Directors (webpage) | nd |

| Eni Trade & Biofuels | ENI – nd – FAQs on Remuneration (webpage) | nd |

| Eni Trade & Biofuels | ENI – nd – Natural gas and LNG (webpage) | nd |

| Eni Trade & Biofuels | ENI – nd – Operations (webpage) | nd |

| Eni Trade & Biofuels | ENI – nd – Organisational Structure | nd |

| Eni Trade & Biofuels | ENI – nd – Our integrated activities (webpage) | nd |

| Eni Trade & Biofuels | ENI – nd – Our relationship with our stakeholders (webpage) | nd |

| Eni Trade & Biofuels | ENI – nd – Parties involved in administration, control or management (webpage) | nd |

| Eni Trade & Biofuels | ENI – nd – Partner selection Process (webpage) | nd |

| Eni Trade & Biofuels | ENI – nd – Poster, How to submit a whistleblowing report | nd |

| Eni Trade & Biofuels | ENI – nd – Privacy Information Anti-Corruption Due Diligence | nd |

| Eni Trade & Biofuels | ENI – nd – Privacy Information Notice on Whistleblowing | nd |

| Eni Trade & Biofuels | ENI – nd – Procurement Internal Website, home page (webpage) | nd |

| Eni Trade & Biofuels | ENI – nd – Statement on Respect for Human Rights | nd |

| Eni Trade & Biofuels | ENI – nd – Supplier Code of Conduct | nd |

| Eni Trade & Biofuels | ENI – nd – Supplier Collaboration (webpage) | nd |

| Eni Trade & Biofuels | ENI – nd – Suppliers FAQs (webpage) | nd |

| Eni Trade & Biofuels | ENI – nd – The Sustainability and Scenarios Committee (webpage) | nd |

| Eni Trade & Biofuels | ENI – nd – Trading and Shipping Activities (webpage) | nd |

| Eni Trade & Biofuels | ENI – nd – Trading and Shipping, the REACH, REMIT and EMIR (webpage) | nd |

| Eni Trade & Biofuels | ENI – nd – Transparency (webpage) | nd |

| Eni Trade & Biofuels | ENI – nd – Whistleblowing Report Form (webpage) | nd |

| Eni Trade & Biofuels | ENI – nd – Rules of the Control and Risk Committee | nd |

| ExxonMobil | Exxonmobil – 2022 – Advancing Climate Solutions Progress Report | 2022 |

| ExxonMobil | ExxonMobil – 2022 – Audit Committee Charter (webpage) | 2022 |

| ExxonMobil | ExxonMobil – 2022 – Board of Directors (webpage) | 2022 |

| ExxonMobil | ExxonMobil – 2022 – Canada Lobbyists Registration System | 2022 |

| ExxonMobil | ExxonMobil – 2022 – Code of Ethics (webpage) | 2022 |

| ExxonMobil | ExxonMobil – 2022 – Crude trading (webpage) | 2022 |

| ExxonMobil | ExxonMobil – 2022 – Energy & Carbon Summary (webpage) | 2022 |

| ExxonMobil | ExxonMobil – 2022 – Environmental management (webpage) | 2022 |

| ExxonMobil | ExxonMobil – 2022 – EU Transparency Register (webpage) | 2022 |

| ExxonMobil | ExxonMobil – 2022 – EU Transparency Register, List of Meetings with European Commission since 2014 | 2022 |

| ExxonMobil | ExxonMobil – 2022 – Human Rights (webpage) | 2022 |

| ExxonMobil | ExxonMobil – 2022 – Notice of 2022 Annual Meeting and Proxy Statement | 2022 |

| ExxonMobil | ExxonMobil – 2022 – OIMS Framework Brochure | 2022 |

| ExxonMobil | ExxonMobil – 2022 – Public Issues and Contributions Committee Charter (webpage) | 2022 |

| ExxonMobil | ExxonMobil – 2022 – Supplier, vendor and contractor expectations (webpage) | 2022 |

| ExxonMobil | ExxonMobil – 2022 – Supply chain management (webpage) | 2022 |

| ExxonMobil | ExxonMobil – 2022 – Water management (webpage) | 2022 |

| ExxonMobil | ExxonMobil – 2021 – Annual Report | 2021 |

| ExxonMobil | ExxonMobil – 2021 – Energy and Carbon Summary | 2021 |

| ExxonMobil | ExxonMobil – 2021 – Financial and Operating Data | 2021 |

| ExxonMobil | ExxonMobil – 2021 – Form 10-K | 2021 |

| ExxonMobil | ExxonMobil – 2021 – US House Q4 Lobbying Report | 2021 |

| ExxonMobil | ExxonMobil – 2020 – Annual Meeting of Shareholders, Supplemental Response | 2020 |

| ExxonMobil | ExxonMobil – 2020 – Board of Directors (webpage) | 2020 |

| ExxonMobil | ExxonMobil – 2020 – Conflict Minerals (webpage) | 2020 |

| ExxonMobil | ExxonMobil – 2020 – Corporate governance guidelines and additional policies (webpage) | 2020 |

| ExxonMobil | ExxonMobil – 2020 – Corporate officers and affiliated companies (webpage) | 2020 |

| ExxonMobil | ExxonMobil – 2020 – Energy and Carbon Summary | 2020 |

| ExxonMobil | ExxonMobil – 2020 – EU Transparency Register (webpage) | 2020 |

| ExxonMobil | ExxonMobil – 2020 – EU Transparency Register, List of Meetings with European Commission since 2014 | 2020 |

| ExxonMobil | ExxonMobil – 2020 – Human rights (webpage) | 2020 |

| ExxonMobil | ExxonMobil – 2020 – Investor Presentation | 2020 |

| ExxonMobil | ExxonMobil – 2020 – Lobbying Report Q1 2020 | 2020 |

| ExxonMobil | ExxonMobil – 2020 – Notice of 2020 Annual Meeting and Proxy Statement | 2020 |

| ExxonMobil | ExxonMobil – 2020 – Political contributions and lobbying (webpage) | 2020 |

| ExxonMobil | ExxonMobil – 2020 – Presentation, Investor Day | 2020 |

| ExxonMobil | ExxonMobil – 2020 – Statement on labor and the workplace (webpage) | 2020 |

| ExxonMobil | ExxonMobil – 2020 – US House of Representative, Lobbying Disclosure, 2nd quarter report | 2020 |

| ExxonMobil | ExxonMobil – 2020 – US PAC Contributions | 2020 |

| ExxonMobil | ExxonMobil – XTO – 2020 – Pipelines Public Awareness (webpage) | 2020 |

| ExxonMobil | ExxonMobil – 2020 – Sustainability Report Highlights | 2020 |

| ExxonMobil | ExxonMobil – 2020 – Sustainability Report Human Rights | 2020 |

| ExxonMobil | ExxonMobil – 2020 – UK Tax Strategy (webpage) | 2020 |

| ExxonMobil | ExxonMobil – 2019 – Corporate Political Contributions to State Candidates and Committees | 2019 |

| ExxonMobil | ExxonMobil – 2019 – EU Policy principles (webpage) | 2019 |

| ExxonMobil | ExxonMobil – 2019 – EU policy recommendations (webpage) | 2019 |

| ExxonMobil | ExxonMobil – 2019 – Executive Compensation Overview | 2019 |

| ExxonMobil | ExxonMobil – 2019 – Financial and Operating Data | 2019 |

| ExxonMobil | ExxonMobil – 2019 – Financial Statement and Supplemental Information | 2019 |

| ExxonMobil | ExxonMobil – 2019 – Form 10K, Annual Report | 2019 |

| ExxonMobil | ExxonMobil – 2019 – Global energy trade, creating a robust network (webpage) | 2019 |

| ExxonMobil | ExxonMobil – 2019 – Lobbying Contribution Report H2 2019 | 2019 |

| ExxonMobil | ExxonMobil – 2019 – Outlook for Energy | 2019 |

| ExxonMobil | ExxonMobil – 2019 – Summary Annual Report | 2019 |

| ExxonMobil | ExxonMobil – 2019 – Supplier, vendor and contractor expectations (webpage) | 2019 |

| ExxonMobil | ExxonMobil – 2019 – Worldwide Giving Report 2018 (webpage) | 2019 |

| ExxonMobil | ExxonMobil – XTO – 2019 – Pipeline Safety and Operations (webpage) | 2019 |

| ExxonMobil | ExxonMobil – XTO – 2019 – Year-End Supplier Communications (webpage) | 2019 |

| ExxonMobil | ExxonMobil – 2018 – Business divisions (webpage) | 2018 |

| ExxonMobil | ExxonMobil – 2018 – LNG Global Portfolio (webpage) | 2018 |

| ExxonMobil | ExxonMobil – 2018 – Our guiding principles (webpage) | 2018 |

| ExxonMobil | ExxonMobil – 2018 – Our history (webpage) | 2018 |

| ExxonMobil | ExxonMobil – 2018 – SEC Exhibit 21, Subsidiaries of the Registrant (webpage) | 2018 |

| ExxonMobil | ExxonMobil – 2018 – Socioeconomic Management Standard (webpage) | 2018 |

| ExxonMobil | ExxonMobil – 2018 – Sustainability Report Highlights | 2018 |

| ExxonMobil | ExxonMobil – 2018 – Sustainability Report, Content Index (webpage) | 2018 |

| ExxonMobil | ExxonMobil – 2018 – Sustainability Report, Human Rights (webpage) | 2018 |

| ExxonMobil | ExxonMobil – 2018 – Sustainability Report, Reporting Guidelines and Legal Information (webpage) | 2018 |

| ExxonMobil | ExxonMobil – 2018 – Sustainability Report, Safety (webpage) | 2018 |

| ExxonMobil | ExxonMobil – 2018 – Sustainability Report, Shareholder relations (webpage) | 2018 |

| ExxonMobil | ExxonMobil – 2018 – Sustainability Report, Supply chain management (webpage) | 2018 |

| ExxonMobil | ExxonMobil – 2018 – Sustainability Report, Working with local communities (webpage) | 2018 |

| ExxonMobil | ExxonMobil – 2018 – Sustainable water solutions, public policy considerations (webpage) | 2018 |

| ExxonMobil | ExxonMobil – 2018 – Transparency and anti-corruption (webpage) | 2018 |

| ExxonMobil | ExxonMobil – 2018 – U.S. energy policy changes could create thousands of jobs (webpage) | 2018 |

| ExxonMobil | ExxonMobil – 2018 – Worldwide Contributions and Community Investments | 2018 |

| ExxonMobil | ExxonMobil – Mobil Trading and Supply Limited – 2018 – Slavery and human trafficking statement | 2018 |

| ExxonMobil | ExxonMobil – 2018 – Operations Integrity Management System Chairmans message (webpage) | 2018 |

| ExxonMobil | ExxonMobil – 2018 – Putting OIMS into practice (webpage) | 2018 |

| ExxonMobil | ExxonMobil – 2017 – Board Affairs Committee Charter (webpage) | 2017 |

| ExxonMobil | ExxonMobil – 2017 – Global Diversity Booklet | 2017 |

| ExxonMobil | ExxonMobil – 2017 – Standards of Business Conduct | 2017 |

| ExxonMobil | ExxonMobil – 2017 – Sustainability Report Highlights | 2017 |

| ExxonMobil | ExxonMobil – 2016 – Guidelines for the Selection of Non-employee Directors (webpage) | 2016 |

| ExxonMobil | ExxonMobil – 2016 – Procedures for Shareholders and Other Interested Parties to Communicate to the Non-Employee Directors (webpage) | 2016 |

| ExxonMobil | ExxonMobil – 2016 – Progress Through Partnership | 2016 |

| ExxonMobil | ExxonMobil – 2016 – Wholesale Fuel Sales and Services | 2016 |

| ExxonMobil | ExxonMobil – 2014 – Anti-Corruption Legal Compliance Guide | 2014 |

| ExxonMobil | ExxonMobil – 2014 – Antiboycott Legal Compliance Guide | 2014 |

| ExxonMobil | ExxonMobil – 2014 – Antitrust and Competition Law Legal Compliance Guide | 2014 |

| ExxonMobil | ExxonMobil – 2014 – Guidelines for Review of Related Person Transactions (webpage) | 2014 |

| ExxonMobil | ExxonMobil – 2011 – Executive Committee Charter (webpage) | 2011 |

| ExxonMobil | ExxonMobil – 2010 – Political Activities Policies and Guidelines | 2010 |

| ExxonMobil | ExxonMobil – 2009 – Finance Committee Charter (webpage) | 2009 |

| ExxonMobil | ExxonMobil – 2009 – Operations Integrity Management System | 2009 |

| ExxonMobil | ExxonMobil – 2007 – Board Statement on Incentive Compensation in Case of Restatement (webpage) | 2007 |

| ExxonMobil | ExxonMobil – 2001 – Certificate of incorporation and by-laws (webpage) | 2001 |

| ExxonMobil | ExxonMobil – LNG – nd – A Global Presence (webpage) | nd |

| ExxonMobil | ExxonMobil – LNG – nd – LNG leadership and team (webpage) | nd |

| ExxonMobil | ExxonMobil – LNG – nd – Sustained growth in the LNG industry (webpage) | nd |

| ExxonMobil | ExxonMobil – nd – Code of Ethics (webpage) | nd |

| ExxonMobil | ExxonMobil – nd – Crude Trading (webpage) | nd |

| ExxonMobil | ExxonMobil – nd – Global Operations (webpage) | nd |

| ExxonMobil | ExxonMobil – nd – LNG, Fueling the Future | nd |

| ExxonMobil | ExxonMobil – nd – Management committee (webpage) | nd |

| ExxonMobil | ExxonMobil – nd – Socioeconomic Management | nd |

| Gerald Group | Gerald Group – 2022 – Find Us (website) | 2022 |

| Gerald Group | Gerald Group – 2022 – Gerald Group Joine Responsible Minerals Initiative | 2022 |

| Gerald Group | Gerald Group – 2022 – Modern Slavery Act Statement (webpage) | 2022 |

| Gerald Group | Gerald Group – 2022 – Sustainability Policy | 2022 |

| Gerald Group | Gerald Group – 2022 – US Lobbying Report LD-2 Disclosure Form (Q2) | 2022 |

| Gerald Group | Gerald Group – 2022 – US Lobbying Report LD-2 Disclosure Form (Q3) | 2022 |

| Gerald Group | Gerald Group – 2021 – Gerald Group Tin ITSCI Report | 2021 |

| Gerald Group | Gerald Group – 2021 – Press Release Marampa Mines Iron Ore from Sierra Leone | 2021 |

| Gerald Group | Gerald Group – 2021 – Press Release new senior women executives | 2021 |

| Gerald Group | Gerald Group – 2021 – Press Release Sierra Leone and Gerald Group announce Marampa Project (webpage) | 2021 |

| Gerald Group | Gerald Group – 2020 – Tax Strategy | 2020 |

| Gerald Group | Gerald Group – 2019 – Health & Safety, Environment and Community Report | 2019 |

| Gerald Group | Gerald Group – 2019 – Health, Safety, Environment & Communities (webpage) | 2019 |

| Gerald Group | Gerald Group – 2019 – Summary Code of Conduct | 2019 |

| Gerald Group | Gerald Group – 2019 – Tin ITSCI Report | 2019 |

| Gerald Group | Gerald Group – 2019 – Summary Policy Health, Safety, Environment and Communities | 2019 |

| Gerald Group | Gerald Group – 2018 – Press Release, Establishment of Gerald International Ltd (webpage) | 2018 |

| Gerald Group | Gerald Group – 2015 – Modern Slavery Act Statement (webpage) | 2015 |

| Gerald Group | Gerald Group – nd – Group Profile (webpage) | nd |

| Gerald Group | Gerald Group – nd – Responsible Metals Trading | nd |

| Glencore | Glencore – 2022 – Australian Government Lobbyist Register | 2022 |

| Glencore | Glencore – 2022 – Contract Transparency (webpage) | 2022 |

| Glencore | Glencore – 2022 – Ethics and Compliance Programme | 2022 |

| Glencore | Glencore – 2022 – EU Transparency Register | 2022 |

| Glencore | Glencore – 2022 – Group Entities (webpage) | 2022 |

| Glencore | Glencore – 2022 – Investigations (webpage) | 2022 |

| Glencore | Glencore – 2022 – LME Approved brands | 2022 |

| Glencore | Glencore – 2022 – Lobbying (webpage) | 2022 |

| Glencore | Glencore – 2022 – Our Approach to Transparency (webpage) | 2022 |

| Glencore | Glencore – 2022 – Regulatory News Service (webpage) | 2022 |

| Glencore | Glencore – 2022 – Suplier Code of Conduct | 2022 |

| Glencore | Glencore – 2022 – Third Quarter Production Report | 2022 |

| Glencore | Glencore – 2022 – Transparency CEO Quote (webpage) | 2022 |

| Glencore | Glencore – 2022 – US Senate lobbying disclosure | 2022 |

| Glencore | Glencore – 2022 – World map (webpage) | 2022 |

| Glencore | Glencore – 2022 – World map marketing offices (webpage) | 2022 |

| Glencore | Glencore – 2021 – Answers to Clarification Questions III | 2021 |

| Glencore | Glencore – 2021 – Joint Venture beneficial ownership (webpage) | 2021 |

| Glencore | Glencore – 2021 – Annual Report | 2021 |

| Glencore | Glencore – 2021 – Anti Money Laundering Policy | 2021 |

| Glencore | Glencore – 2021 – Anti-Corruption and Bribery Policy | 2021 |

| Glencore | Glencore – 2021 – Climate Change Report | 2021 |

| Glencore | Glencore – 2021 – Code of Conduct | 2021 |

| Glencore | Glencore – 2021 – Corporate Communications Policy | 2021 |

| Glencore | Glencore – 2021 – EITI Statement by Companies, Beneficial Ownership Transparency Forum | 2021 |

| Glencore | Glencore – 2021 – Environmental Policy | 2021 |

| Glencore | Glencore – 2021 – Ethics and Compliance Report | 2021 |

| Glencore | Glencore – 2021 – Extended ESG Data 2021 | 2021 |

| Glencore | Glencore – 2021 – Fraud Policy | 2021 |

| Glencore | Glencore – 2021 – Full Year Production Report | 2021 |

| Glencore | Glencore – 2021 – Health and Safety Policy | 2021 |

| Glencore | Glencore – 2021 – Human Rights Policy | 2021 |

| Glencore | Glencore – 2021 – Kamoto Copper Company (KCC) Responsible Mineral Supply Chains Report 2021 | 2021 |

| Glencore | Glencore – 2021 – Market Conduct Policy | 2021 |

| Glencore | Glencore – 2021 – Modern Slavery Statement | 2021 |

| Glencore | Glencore – 2021 – Payments to Governments Report | 2021 |

| Glencore | Glencore – 2021 – Political Engagement Policy | 2021 |

| Glencore | Glencore – 2021 – Reporting Criteria for Selected KPIs | 2021 |

| Glencore | Glencore – 2021 – Responsible Sourcing Policy | 2021 |

| Glencore | Glencore – 2021 – Sanctions Policy | 2021 |

| Glencore | Glencore – 2021 – Social Performance Policy | 2021 |

| Glencore | Glencore – 2021 – Sustainability Report | 2021 |

| Glencore | Glencore – 2021 – Tax Policy | 2021 |

| Glencore | Glencore – 2021 – UNGC Communication on Progress | 2021 |

| Glencore | Glencore – 2021 – Whistleblowing Policy | 2021 |

| Glencore | Glencore – Minara Resources – 2021 – Public Due Diligence Report 2021 | 2021 |

| Glencore | Glencore – 2020 – Answers to Clarification Questions | 2020 |

| Glencore | Glencore – 2020 – Answers to Clarification Questions II | 2020 |

| Glencore | Glencore – 2020 – EU Transparency Register (webpage) | 2020 |

| Glencore | Glencore – 2020 – Presentation, Investor Update | 2020 |

| Glencore | Glencore – 2020 – Q3 Production Report | 2020 |

| Glencore | Glencore – 2020 – Supplier Standard | 2020 |

| Glencore | Glencore – 2020 – Supply Chain Due Diligence Overview | 2020 |

| Glencore | Glencore – 2020 – ESG data book and GRI index | 2020 |

| Glencore | Glencore – 2020 – Kamoto Copper Company (KCC) Public Due Diligence Report 2020 | 2020 |

| Glencore | Glencore – 2019 – Annual report | 2019 |

| Glencore | Glencore – 2019 – Climate Change Position Statement | 2019 |

| Glencore | Glencore – 2019 – Environmental, Social and Governance data | 2019 |

| Glencore | Glencore – 2019 – Group Tax Policy | 2019 |

| Glencore | Glencore – 2019 – Human Rights Report | 2019 |

| Glencore | Glencore – 2019 – Modern Slavery Statement | 2019 |

| Glencore | Glencore – 2019 – Payments to Governments Report | 2019 |

| Glencore | Glencore – 2019 – Presentation, SRI rating agencies webinar | 2019 |

| Glencore | Glencore – 2019 – Risk Factors reproduced from the EMTN Base Prospectus | 2019 |

| Glencore | Glencore – 2019 – Sustainability Report | 2019 |

| Glencore | Glencore – 2018 – Code of Conduct | 2018 |

| Glencore | Glencore – 2018 – Global Anti-Corruption Policy | 2018 |

| Glencore | Glencore – 2018 – Sustainability Report | 2018 |

| Glencore | Glencore – 2018 – United Nations Global Compact, Communication on Progress | 2018 |

| Glencore | Glencore – 2017 – Sustainability Policy | 2017 |

| Glencore | Glencore – 2017 – Sustainability Report | 2017 |

| Glencore | Glencore – Glencore Holdings Australia – nd – Australian Government Lobbyist Register | nd |

| Glencore | Glencore – nd – Annex, draft contract clauses | nd |

| Glencore | Glencore – nd – EQS Integrity Line (webpage) | nd |

| Glencore | Glencore – nd – Human Rights Policy | nd |

| Glencore | Glencore – nd – List of associations and memberships | nd |

| Glencore | Glencore – nd – Our approach to Sustainability | nd |

| Glencore | Glencore – nd – Our approach to transparency (webpage) | nd |

| Glencore | Glencore – nd – Suppliers FAQs (webpage) | nd |

| Glencore | Glencore – nd – Suppliers, Our expectations (webpage) | nd |

| Glencore | Glencore – nd – Sustainability, Community and human rights (webpage) | nd |

| Glencore | Glencore – nd – Sustainability, Our approach to sustainability (webpage) | nd |

| Glencore | Glencore – nd – Sustainability, Responsible Sourcing and Supply (webpage) | nd |

| Glencore | Glencore – nd – Terms of Reference Ethics, Compliance and Culture Committee | nd |

| Glencore | Glencore – nd – Terms of reference Health, Safety, Environment and Communities Committee | nd |

| Glencore | Glencore – nd – What we do, Marketing (webpage) | nd |

| Glencore | Glencore – nd – Who we are, Governance, Compliance (Webpage) | nd |

| Glencore | Glencore – nd – Who we are, Governance, Reporting Misconduct (webpage) | nd |

| Glencore | Glencore – nd – Who we are, Transparency (webpage) | nd |

| Glencore | Glencore – nd – World map (webpage) | nd |

| Gunvor | Gunvor – 2022 – A Global Business (webpage) | 2022 |

| Gunvor | Gunvor – 2022 – Business Register Excerpt | 2022 |

| Gunvor | Gunvor – 2022 – Careers (webpage) | 2022 |

| Gunvor | Gunvor – 2022 – Compliance & Ethics (webpage) | 2022 |

| Gunvor | Gunvor – 2022 – Group Brochure | 2022 |

| Gunvor | Gunvor – 2022 – GTR – As deadline looms, some traders remain wary of russia oil price cap (webpage) | 2022 |

| Gunvor | Gunvor – 2022 – H1 2022 Results (webpage) | 2022 |

| Gunvor | Gunvor – 2022 – Leadership (Torbjörn Törnqvist) (webpage) | 2022 |

| Gunvor | Gunvor – 2022 – Leadership (webpage) | 2022 |

| Gunvor | Gunvor – 2022 – Pipelines & Storage (webpage) | 2022 |

| Gunvor | Gunvor – 2022 – Refineries (tab 1) (webpage) | 2022 |

| Gunvor | Gunvor – 2022 – Refineries (tab 2) (webpage) | 2022 |

| Gunvor | Gunvor – 2022 – Statement regarding the war in Ukraine (webpage) | 2022 |

| Gunvor | Gunvor – 2022 – Terminals (tab 1) (webpage) | 2022 |

| Gunvor | Gunvor – 2022 – Terminals (tab 2) (webpage) | 2022 |

| Gunvor | Gunvor – 2022 – Terminals (tab 3) (webpage) | 2022 |

| Gunvor | Gunvor – 2021 – Sustainability, Ethics & Compliance Report | 2021 |

| Gunvor | Gunvor – 2020 – HSEC Governance Framework | 2020 |

| Gunvor | Gunvor – 2020 – Sustainability, Ethics & Compliance Report | 2020 |

| Gunvor | Gunvor – 2019 – Compliance Factsheet | 2019 |

| Gunvor | Gunvor – 2019 – Group Summary | 2019 |

| Gunvor | Gunvor – 2019 – News Release, Group Results (webpage) | 2019 |

| Gunvor | Gunvor – 2019 – Sustainability Ethics & Compliance Report | 2019 |

| Gunvor | Gunvor – 2018 – Code of Conduct Ethics for Business Partners | 2018 |

| Gunvor | Gunvor – 2018 – Group Brochure | 2018 |

| Gunvor | Gunvor – 2018 – News Release, Gunvor closes innovative US745 million Facility linked to Sustainability Targets (webpage) | 2018 |

| Gunvor | Gunvor – 2018 – News Release, Gunvor joins EITI (webpage) | 2018 |

| Gunvor | Gunvor – 2018 – News Release, Gunvor moves to integrate UN Human Rights Principles (webpage) | 2018 |

| Gunvor | Gunvor – 2018 – Payments to Governments, EITI | 2018 |

| Gunvor | Gunvor – 2018 – Sustainability Ethics & Compliance Report | 2018 |

| Gunvor | Gunvor – 2017 – Group Brochure | 2017 |

| Gunvor | Gunvor – 2016 – Independent Inspection Requirements | 2016 |

| Gunvor | Gunvor – 2016 – The Resolution of the Board of Directors on Poland Tariff End Users Gas | 2016 |

| Gunvor | Gunvor – 2015 – Poland Energy Regulatory Office decision in respect of the Tariff for High-Methane Gas (Polish) | 2015 |

| Gunvor | Gunvor – Clearlake Shipping – nd – About Company Profile (webpage) | nd |

| Gunvor | Gunvor – Clearlake Shipping – nd – Compliance (webpage) | nd |

| Gunvor | Gunvor – Clearlake Shipping – nd – HSE (webpage) | nd |

| Gunvor | Gunvor – Gunvor Petroleum Rotterdam – nd – About (webpage) | nd |

| Gunvor | Gunvor – Gunvor Petroleum Rotterdam – nd – HSEC (webpage) | nd |

| Gunvor | Gunvor – nd – Bulk Materials Trade (webpage) | nd |

| Gunvor | Gunvor – nd – Clearlake Shipping – Compliance (webpage) | nd |

| Gunvor | Gunvor – nd – Compliance and Ethics (webpage) | nd |

| Gunvor | Gunvor – nd – Crude Oil Trade (webpage) | nd |

| Gunvor | Gunvor – nd – Health & Safety (webpage) | nd |

| Gunvor | Gunvor – nd – Investments in Pipelines & Storage (webpage) | nd |

| Gunvor | Gunvor – nd – Leadership (webpage) | nd |

| Gunvor | Gunvor – nd – Product Safety (webpage) | nd |

| Gunvor | Gunvor – nd – Refined Products & Energy Trade (webpage) | nd |

| Gunvor | Gunvor – nd – Risk Management (webpage) | nd |

| LITASCO | LITASCO – 2022 – Contacts (webpage) | 2022 |

| LITASCO | LITASCO – 2022 – General Information (webpage) | 2022 |

| LITASCO | LITASCO – 2022 – LITASCO SA (webpage) | 2022 |

| LITASCO | LITASCO – 2022 – Support functions (webpage) | 2022 |

| LITASCO | LUKOIL – 2022 – Board of Directors (webpage) | 2022 |

| LITASCO | LUKOIL – 2022 – Clean water (webpage) | 2022 |

| LITASCO | LUKOIL – 2022 – Energy efficiency (webpage) | 2022 |

| LITASCO | LUKOIL – 2022 – Ethics (webpage) | 2022 |

| LITASCO | LUKOIL – 2022 – Group Sustainability Policy | 2022 |

| LITASCO | LUKOIL – 2022 – Human rights (webpage) | 2022 |

| LITASCO | LUKOIL – 2022 – International Projects (webpage) | 2022 |

| LITASCO | LUKOIL – 2022 – Reuters: Three foreign representatives quit board of Russias Lukoil (webpage) | 2022 |

| LITASCO | LUKOIL – 2022 – Supply chain (webpage) | 2022 |

| LITASCO | LUKOIL – 2022 – Tax policy (webpage) | 2022 |

| LITASCO | LUKOIL – 2022 – Wholesale and Trading (webpage) | 2022 |

| LITASCO | LUKOIL – 2021 – Annual Report of PJSC Lukoil | 2021 |

| LITASCO | LUKOIL – 2021 – CDP Climate Change Report | 2021 |

| LITASCO | LUKOIL – 2021 – Consolidated Financials | 2021 |

| LITASCO | LUKOIL – 2021 – Group Sustainability Report | 2021 |

| LITASCO | LUKOIL – 2021 – MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL | 2021 |

| LITASCO | Litasco – 2020 – Response to clarification Questions | 2020 |

| LITASCO | Lukoil – 2020 – Analyst Databook Q2 | 2020 |

| LITASCO | Lukoil – 2020 – Annual General Shareholders Meeting Materials | 2020 |

| LITASCO | Lukoil – 2020 – Anti-Corruption Policy | 2020 |

| LITASCO | Lukoil – 2020 – Ecological Culture | 2020 |

| LITASCO | Lukoil – 2020 – Health, Safety and Environmental Policy of Lukoil Group in the 21st Century | 2020 |